The US, once a global leader in aluminum production, now produces just 1.2% of the world’s aluminum supply. In 2024, we produced a mere 680,000 tons, or 50% of demand in the US.

The US imported over 4.8 million tons of ingot and billet last year — and Canada alone supplied 2.6 million tons of that total.

Our number one trading partner for this commodity is Canada. Statistically, Mexico was not even on the map.

Why? The cost of energy. Aluminium smelting is incredibly energy-intensive, with electricity often accounting for up to half of production expenses.

In the US, industrial electricity prices are significantly higher than in Canada, where most aluminum smelters are concentrated in Quebec. Thanks to abundant, low-cost hydroelectric power, Canadian smelters enjoy energy costs up to three times lower than their US counterparts.

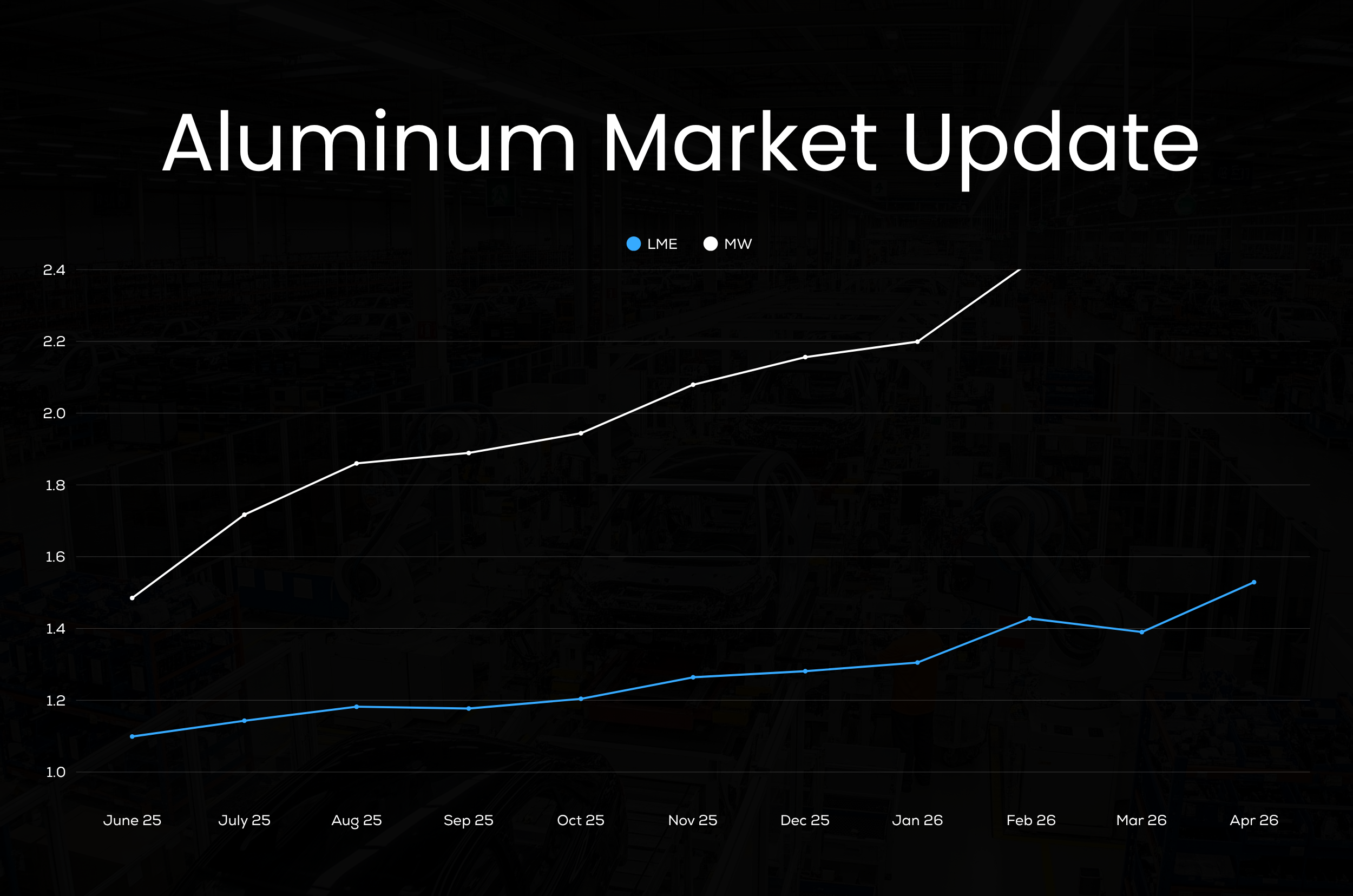

If tariffs are fully implemented, prices for aluminum, raw and processed, will increase worldwide. Domestic extrusion mills have already notified customers of impending increases.

Why Aluminum Prices Continue to Rise

The current aluminum price spike is being driven much more by supply disruption than demand growth. Middle East Supply Shock